Not known Facts About Mortgage

Governments usually regulate several aspects of home loan borrowing, either directly (through lawful needs, as an example) or indirectly (via regulation of the individuals or the monetary markets, such as the financial sector), as well as usually with state intervention (direct borrowing by the government, direct financing by state-owned financial institutions, or sponsorship of various entities) - Mortgage.

Mortgage are normally structured as lasting car loans, the regular payments for which resemble an annuity as well as calculated according to the time worth of cash formulae - Mortgage Lender. The most fundamental setup would require a taken care of monthly payment over a period of 10 to thirty years, depending upon local problems.

Home mortgage lending will certainly likewise take into consideration the (regarded) riskiness of the mortgage, that is, the chance that the funds will be settled (normally considered a function of the credit reliability of the consumer); that if they are not settled, the loan provider will be able to seize on the genuine estate possessions; and the economic, passion rate risk as well as time delays that may be entailed in particular circumstances - Mortgage Lender.

The Main Principles Of Interest Rates

There are many kinds of home loans used worldwide, however numerous factors generally define the features of the mortgage. Every one of these may go through regional regulation as well as legal needs. Interest: Passion might be repaired for the life of the funding or variable, as well as change at certain pre-defined durations; the interest rate can likewise, obviously, be higher or reduced.

Both fundamental kinds of amortized lendings are the fixed price home loan (FRM) and also variable-rate mortgage (ARM) (also called a floating price or variable price mortgage) - Mortgage. In some countries, such as the USA, taken care of price mortgages are the standard, yet drifting price home loans are reasonably typical. Combinations of repaired and floating price home loans are also common, where a home loan Related Site will have a set price for some period, as an example the very first five years, and differ after the end of that period.

When it comes to an annuity settlement plan, the regular repayment continues to be the very same amount throughout the loan. When it comes to linear repayment, the regular repayment will progressively decrease. In an adjustable-rate mortgage, the rates of interest is generally fixed for a period of time, after which it will occasionally (as an example, every year or monthly) change up or down to some market index.

Since the threat is transferred to the consumer, the preliminary rates of interest may be, as an example, 0.5% to 2% lower than the average 30-year fixed price; the size of the rate differential will certainly be associated with debt market problems, including the yield curve. The charge to the consumer depends upon the credit history threat along with the interest rate threat.

Interest Rates Things To Know Before You Buy

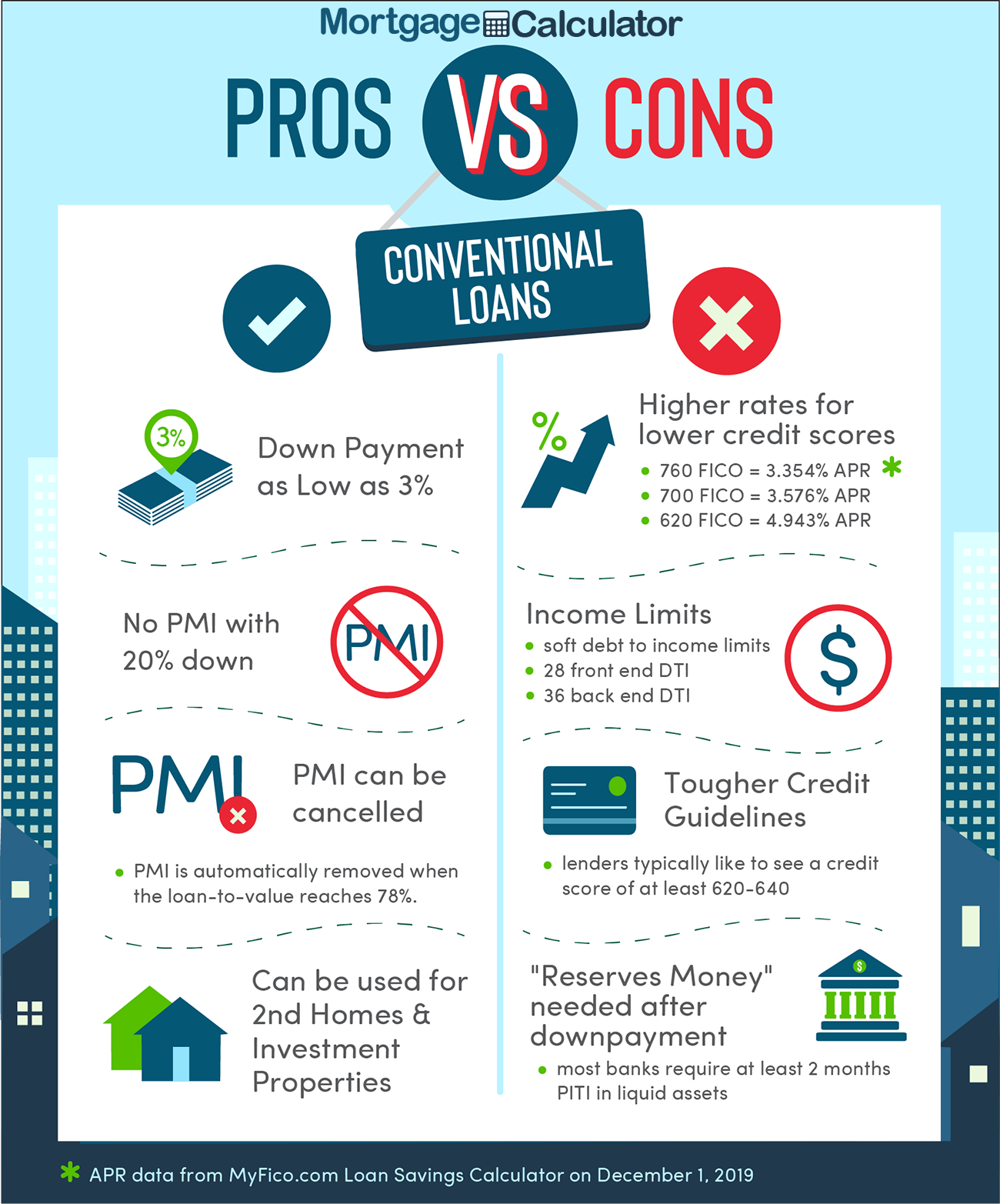

Jumbo mortgages as well as subprime borrowing are not supported by government warranties and deal with higher interest rates. Other advancements explained listed below can affect the rates too. Upon making a home mortgage see here now lending for the purchase of a residential or commercial property, lenders typically require that the borrower make a down repayment; that is, contribute a section of the expense of the property.

The finance to value ratio (or LTV) is the size of the loan versus the value of the residential or commercial property. Consequently, a mortgage in which the purchaser has actually made a deposit of 20% has a car loan to value ratio of 80%. For financings made against residential or commercial properties that the customer currently has, the financing to worth ratio will certainly be imputed versus the estimated value of the building.

Since the value of the residential property is a vital consider understanding the threat of the lending, figuring out the value is a vital variable in home loan lending. The worth may be identified in different ways, but the most typical are: Real or deal worth: this is normally required the purchase cost of the residential or commercial property.

Common denominators include settlement to income (home mortgage settlements as a percent of gross or internet income); debt to revenue (all financial debt settlements, including mortgage repayments, as a percentage of earnings); as well as various internet worth measures. In many countries, credit report are utilized instead of or use this link to supplement these steps.

Home Equity Loans Things To Know Before You Get This

the specifics will vary from place to location. Some loan providers might additionally require a potential consumer have several months of "get assets" readily available. In other words, the debtor may be required to show the accessibility of adequate properties to spend for the housing prices (consisting of home mortgage, tax obligations, and so on) for a time period in case of the job loss or various other loss of earnings.